Table of Contents

A T account is defined as a visual representation of a general ledger account used in double-entry bookkeeping, with debits recorded on the left side and credits on the right side of a T-shaped diagram. T accounts are one of the primary forms of performing double-entry accounting.

Key Takeaways:

- T accounts are simple and easy to use

- Two sides to the account: debit (left) and credit (right)

- T accounts can be very time consuming

- It's more effective to use financial projection software like Baremetrics, to capture all variables and eliminate human error

Last updated: March 2026

Above the T is the name of the account, and the T account is then separated into left (debit) and right (credit) sides.

T accounts are a simple and convenient way to organize your journals for basic bookkeeping functions.

The double-entry system helps prevent errors, while the T accounts can be logically ordered to make it easy to find specific transactions quickly. T accounts are a good supplement to the general ledger, which is defined as the master accounting record that contains all of a company's financial transactions organized by account.

The general ledger and T accounts work as intermediaries between primary documents, such as invoices or receipts, and the financial statements used by financial management, including the balance sheet, statement of cash flows, and income statement.

That makes T accounts a good place to start when thinking about bookkeeping and accounting, but also financial management.

What Are T Accounts?

T accounts are clear, visual representations of a business transactions that take the form of a "T" – one side for debits, one for credits.

T accounts are an easy way to represent a single account. They work with the double-entry accounting system to reduce the chance of errors. They are a visual way of recording all transactions that a company makes.

When I was in business school, T accounts were the first step in learning about accounting. While they can be time consuming, they are simple, and simple is good.

If you are new to bookkeeping, I recommend creating T accounts for all of your accounts, from your different assets and liabilities found on the balance sheet to the revenue and expenses found on the profit and loss statement (also called the income statement).

How Do You Make a T Account?

The basic T account has the following components:

- First, two lines are drawn that look like a T.

- The account title is then written on top of the horizontal line.

- The debit side is on the left.

- The credit side is on the right.

What Does a T Account Look Like?

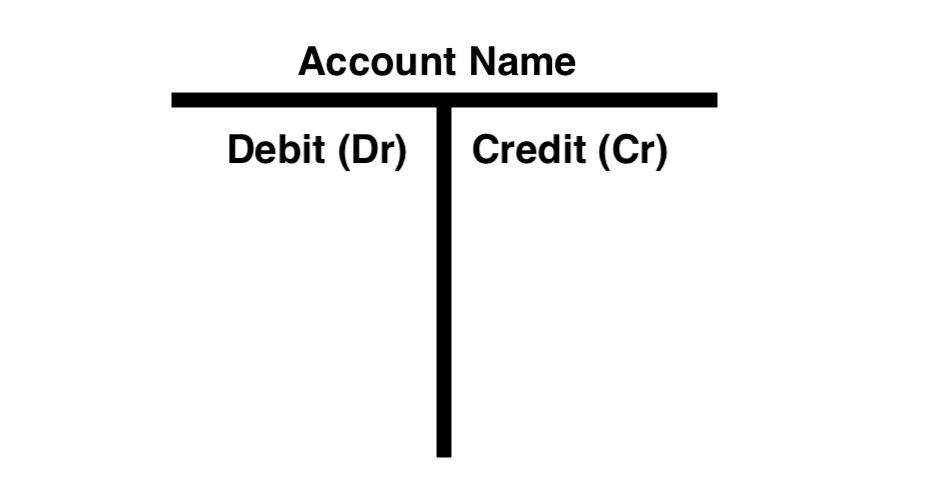

Here is an example of a T Account:

As you can see, the T account gets its name from the two lines that separate the sections. It looks like a T and it is an account, hence T account. Pretty simple, right?!

At the top you have the account name, for example "cash," "owner's equity," or "accounts payable." Then, inside the T, the left side is for debit and the right side for credit transactions.

Some accounts have a debit-side balance, while others have a credit-side balance.

How Do T Accounts Work in Practice?

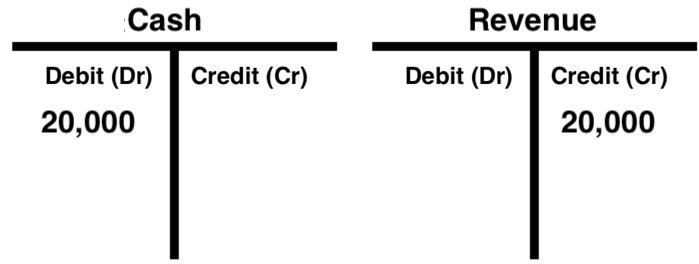

I'm going to go through a really easy example to show double-entry accounting using T accounts in action. Let's say you just sold a one-year premium subscription for $20,000 and your client paid in cash.

Then, the two involved accounts are your cash account and your revenue account.

In this case, you debit $20,000 in the cash T account and credit $20,000 in the revenue T account. Two entries (hence, double entry), one on the left and one on the right, so everything is good.

It really is that simple.

I'm lying. It is this simple for cash accounting, but it isn't for accrual accounting, which you likely use. In accrual accounting, you need to recognize your revenue according to ASC 606, which means you also need to involve a deferred revenue account.

In this case, there'd actually be cash and deferred revenue transactions at first, and then deferred revenue and revenue transactions over time as you recognize the revenue.

How Are the Main Accounts Represented in T Accounts?

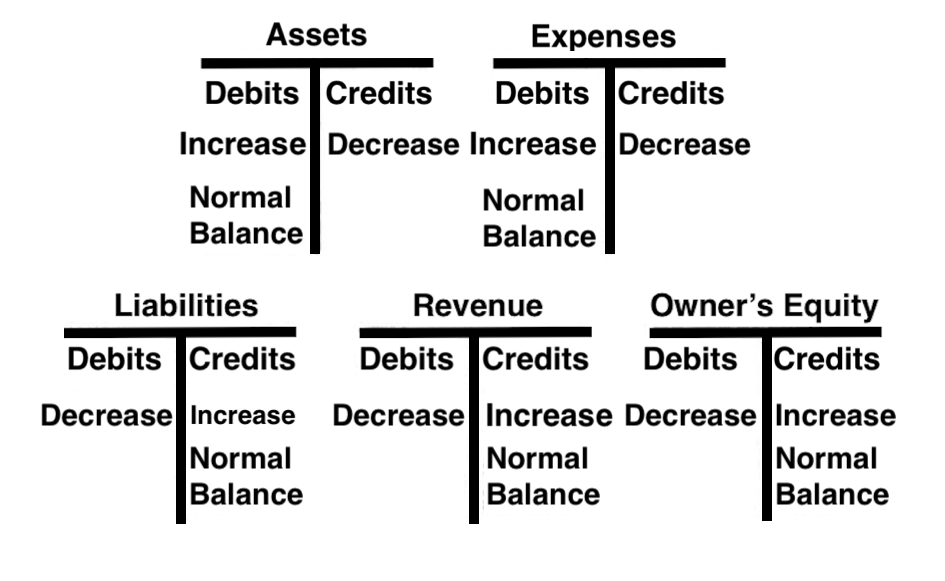

Take a look at the following chart to see where different accounts keep their balances:

As you can see, assets and expenses have normal balances on the left, while liabilities, revenue, and owner's equity have normal balances on the right. As you can see from the chart above, cash normally has a debit-side balance while revenue has a credit-side balance.

I say normal balances because they don't always have balances on those sides—but they should. For example, if your checking account is in overdraft then you have negative cash, which would show a balance on the right side instead. It basically means you have a cash liability instead of asset, which is not good.

Why Do Accountants Use T Accounts?

Remember when I said that T accounts were the first things I learned in accounting classes at business school? Well, that's the primary reason accountants use T accounts specifically. By the time you have an accounting certificate, you have at least a decade of experience using T accounts.

They are simple, easy to read, and generally foolproof. When an accountant is looking for errors, double checking the work of bookkeepers during an audit, or generally wants to be extra sure there are no mistakes, T accounts are the ultimate failsafe tool.

They are often done on paper with a pencil while running through the general ledger in Google Sheets, QuickBooks, Microsoft Excel, or Forecast+ by Baremetrics.

By creating the paper trail between the digital documents on the one side and the receipts, invoices, etc. on the other side, the accountant can be even more sure that the books are in order.

That's why accountants use T accounts specifically, but why do they do any of this at all? It all comes down to the safety afforded by double-entry accounting.

Double-entry accounting is defined as a method of recording every transaction twice to ensure that nothing is missed. Every transaction has two equal parts, a debit one and a credit one.

By recording the debit and credit halves of the transaction and then running a trial balance — which refers to a report that lists all account balances to verify that total debits equal total credits — the accountant can be sure that nothing has been missed. If the books don't balance, then something is wrong, and they need to go find it.

In fact, the error itself usually tells the accountant what is wrong and makes it easier to find the mistake.

What Are the Advantages of T Accounts?

T accounts have two very simple advantages: they are easy and they are clear.

While that might not seem like a lot, it is everything in bookkeeping, especially when you do it alone.

You want a system of bookkeeping that is manageable, especially when you do it in house. By using T accounts and a general ledger, you have simple, generally foolproof record keeping systems in place.

You also want something that can be picked up by anybody and understood. You don't want a tax official, VC, bank, or anyone else confused by your work. The last thing you want is to miss out on a needed loan or investment because someone couldn't understand your books.

What Are the Disadvantages of T Accounts?

The major problem with T accounts is that they are time consuming. You need to set up every account separately and then go through them constantly to record every transaction as it comes in.

You'll also want to then record every transaction again in your general ledger to have all transactions in one place.

Doing two sets of double-entry accounting is a great way to make sure your books are complete and accurate, but it is also time consuming.

That's why we recommend connecting your QuickBooks account to Forecast+ by Baremetrics.

Use Baremetrics to Track Your T Accounts

Maintaining easy-to-read, detailed, accurate, and compliant books is a challenge. At best, it is a distraction from your busy schedule. At worse, it can lead to an audit and expensive tax trouble in the future.

Well organized T accounts are the first step in the bookkeeping and accounting process. If they are inaccurate or hard to follow, then everything from drafting financial statements to forecasting future revenue growth is in jeopardy.

That's where Baremetrics comes in. Simply connect your account to QuickBooks or upload a .csv file and everything from your T accounts is there for you.

To start modeling your finances and effectively operate your business, import your bookkeeping and accounting into Baremetrics. Get accounting and business metrics all at once.

Forecast Financial Data with Baremetrics

Whether you use T accounts, a general ledger, or both to record every transaction, that's only the start of monitoring and forecasting your financials. These are essential elements of the continued success of any business.

That's why you should use Baremetrics.

Baremetrics helps you create financial statements to ensure accounting compliance. Then, it takes that information, and any specific guidance you choose to input, to provide flexible financial forecasting.

Tired of wasting countless hours on spreadsheets? Start your free trial today.